It’s never been easier to pay attention to everything that’s going on with the markets, economy, individual companies or your own portfolio.

People used to get their paper statements in the mail on a monthly basis to know what was going on with their investments. Now we can watch the changes in market values instantaneously.

So it’s more important than ever to filter out the stuff you shouldn’t care about as an investor. Here are 10 things that fit the bill:

1. How rich other people are getting. John Pierpont Morgan is attributed with the quote, “Nothing so undermines your financial judgement as the sight of your neighbor getting rich.”

And JP didn’t have to deal with friends, influencers and celebrities constantly bragging about their lifestyle and wealth on social media all day long. There will always be people with more success, prestige, money and accolades than you.

Easier said than done but not worrying about how much money other people are making can save you a lot of unnecessary stress and angst.

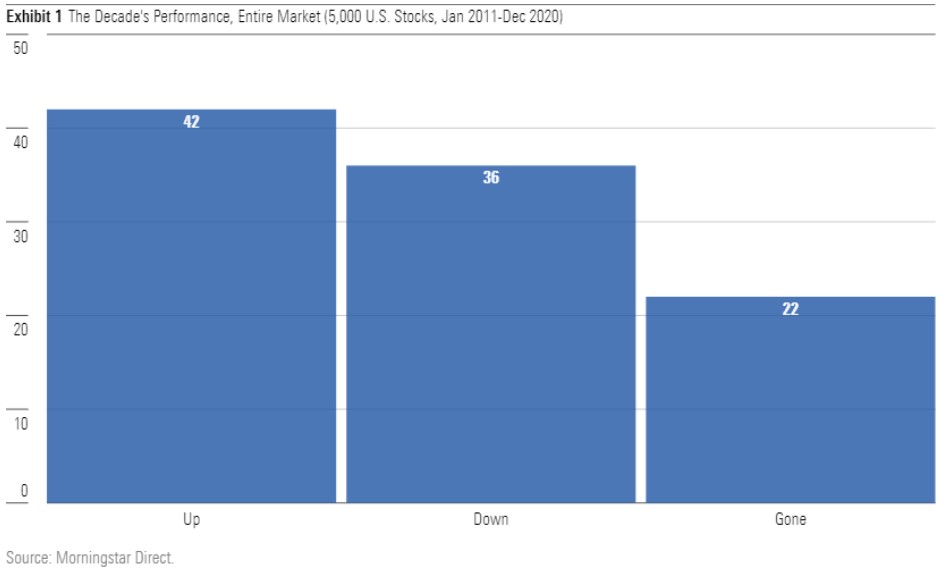

2. What you paid for an investment. Morningstar’s John Rekenthaler recently update the work of Hendrik Bessembinder to show how many stocks outperform the stock market:

Although the stock market itself has been strong, the results for individual companies as a whole are not as good as you would expect in a bull market:

Although the Morningstar U.S. Stock Index enjoyed a 13.90% annualized gain for the decade, only 42% of individual equities finished in the black. Nearly as many (36%) posted 10-year losses. The final 22% vanished. While I did not investigate the fates of the dead, Bessembinder’s research suggests that half the expired stocks were acquired, with decent results, while the other half were delisted, with dire consequences.

Even during a decade marked by an almost uninterrupted bull market, the average stock wasn’t much good.

Picking stocks is harder than you think. Buy and hold is a terrific strategy for some stocks. For others, it’s the equivalent of an investor death sentence.

I’ll just wait until I breakeven is a tough place to be as an investor because some stocks don’t come back…ever.

There’s a fine line between being disciplined and being stubborn when it comes to investing.

3. The amount of time and effort you put into your investments. In many areas of life, trying harder leads to better results. That’s not the case when it comes to investing. In fact, trying harder and paying more attention to your investments will often lead to worse results.

There are no extra points for degree of difficulty when it comes to the markets.

Most investors would be better served doing less, not more.

4. One year performance numbers. One year (or any shorter time frame for that matter) returns don’t tell you anything about yourself as an investor. Every investor will have good years and bad years.

Diversification often looks silly over the short-term. Risk management can seem useless. Luck can trump skill.

You’re probably not as good or as bad as your short-term performance numbers suggest. Long-term returns are the only ones that matter.

5. Your IQ. EQ matters more than IQ when investing.

Yes, some level of intelligence is required but as Warren Buffett once said, “Investing is not a game where the guy with the 160 IQ beats the guy with the 130 IQ. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing.”

There are plenty of intelligent people involved with the markets but not nearly as many who have control over their reactions.

Intelligence alone does not guarantee success in the markets.

6. Financial advice from billionaires. Ultra-successful people typically offer some of the worst financial advice. They’re simply too out of touch with normal people to provide useful advice.

It’s also important to remember these people say stuff all the time that they don’t actually act on. You have to watch what they do, not what they say. And even then, these people don’t know your financial circumstances. How can they possibly offer you actionable advice?

And billionaires have the ability to make huge mistakes with their wealth and they’ll still be fine. If you make a huge mistake it’s going to hurt a lot more.

7. How much you could have made if you would have only put $10k into… I hate these comparisons.

You know, if you would have put $10k into [something that’s up 10,000%] you would be fabulously wealthy.

Oh really, thanks for that. Very helpful. Maybe next time tell me beforehand.

It’s also true that if you put $10k into Enron stock you would have $0 right now.

These fantasies serve no purpose unless you know how to spot them ahead of time.

8. Success in other areas of your life. Your biggest risk as an investor depends a lot on your personality, emotional make-up and station in life.

The biggest risk for most young investors is the fact that they don’t know how they will react under certain market conditions. At a young age, you don’t know how much you don’t know yet and that can come back to bite you.

For more seasoned investors, your experience can actually work against you if it allows you to become overconfident in your own abilities. This is true of people who have found success in other areas of their life as well.

The worst investors are often those who assume success in their career automatically translates to success investing in the markets. It doesn’t work like that.

9. Timing the market perfectly. Investors waste far too much time trying to find the perfect entry point for their investments. That perfect entry point is only known with the benefit of hindsight. You’re far better off putting your money to work when you have some money to put to work and letting compound interest make up for any ill-timed purchases.

Here’s my regular reminder that a long time horizon can trump even the most poorly timed of investments:

It’s fun to look at returns from the tops and bottoms for certain markets or stocks but no one actually invests consistently at the peaks or troughs.

10. Producing alpha in your portfolio. Jason Zweig once told a story about interviewing dozens of residents in Boca Raton, FL, one of the wealthiest retirement communities in the country:

Amid the elegant stucco homes, the manicured lawns, the swaying palm trees, the sun and the sea breezes, I asked these folks — mostly in their seventies — if they’d beaten the market over the course of their investing lifetimes. Some said yes, some said no. Then one man said, “Who cares? All I know is, my investments earned enough for me to end up in Boca.”

No one on their death bed has ever regretted the fact that they didn’t have a better Sharpe ratio.

The whole point of investing in the first place is achieving your financial goals, not beating the market.

Further Reading:

It’s OK to Build Wealth Slowly